Turkey's Central Bank is slightly paralyzed and waits for... global peace

Turkey's Central Bank is slightly paralyzed and waits for... global peace

Erdogan hugs their enemies for other reasons, not to specifically help the CB (#3)

In a series of foreign policy manoeuvres, the president of Turkey seems to have made peace with every leader he was in a war of words in recent years. There are a few exceptions, such as the Egyptian president, but given the pace and strength of his hug with Mohammed bin Salman, it is only a matter of time before Erdogan takes selfies with Abdel Fattah el-Sisi.

In Turkey’s public sphere, some commentators interpret the latest diplomatic initiatives as reflecting the need to find new sources to bail out the construction sector and support the Central Bank, needing new swap agreements. Is it the case?

This takes us to the second part of our mini-series on the creativity and absurd interventions of the Central Bank of Turkey.

In my previous entry, I mentioned that the CB started to record the borrowed USD as net assets in 2018-19. Thanks to the accumulation of off-balance-sheet liabilities, at first sight, the CB seems to have maintained the FX reserves amid the 2018-19 crisis and the Covid-19 pandemic.

The truth is it could not.

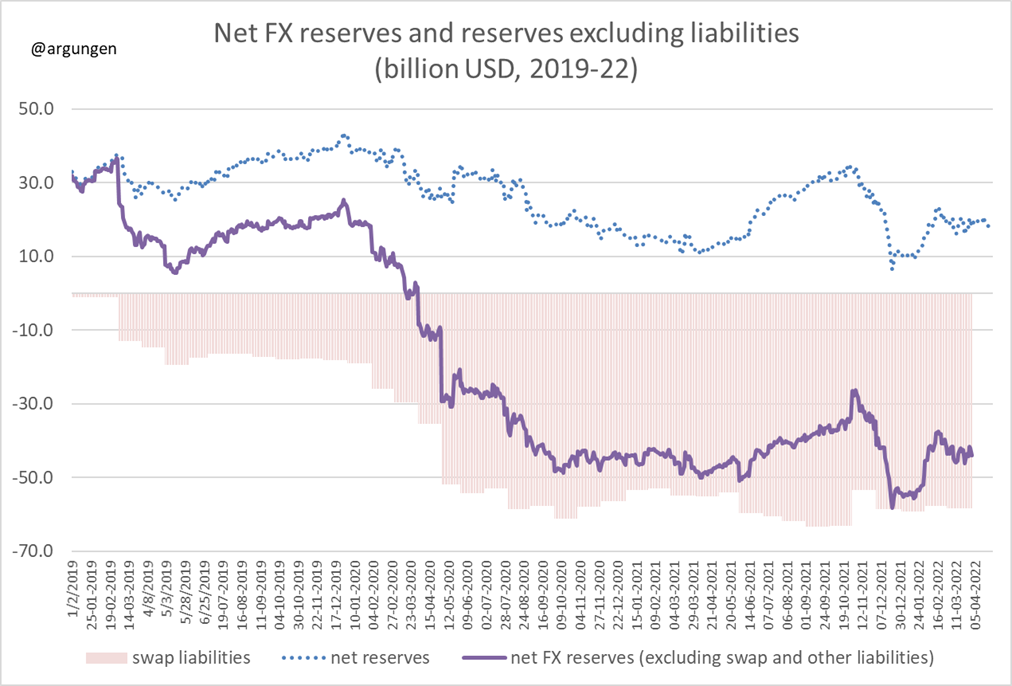

Three moments in the no reserves era

Below I present the net FX reserves presented by the CB, the open position of the CB due to swaps and the net FX reserves minus outstanding swap liabilities and other off-balance sheet liabilities (source: CB Balance Sheet and International Reserves Data).

There have been three significant moments in this no reserves saga. The first one was the 2018-19 crisis and the attempt to avoid currency volatility during the political uncertainty of spring 2019 (see the first part of this series).

The second was the start of the Covid-19 pandemic. The volume of capital outflows from the global South, including Turkey, was comparable to the outflows in the first months of the 2008-09 crisis. Turkish monetary authorities used more of this swap mechanism to mitigate the impact.

Two significant moves aggravated the problem in 2020. The first was the market interventions by both the CB and the public banks in early summer 2020. Reuters estimated that thanks to the FX sales in the first months of the pandemic, and notably June 2020, these operations added up to a volume of 100 billion USD from early 2019 to mid-2020.

The second move was Treasury’s unprecedented FX borrowing in domestic markets. Public banks were the primary buyers of newly issued FX debt, and they used their new assets to aid the CB with the continuity and the deepening of swaps. As a result, the CB kept showing the net reserves at a higher rate, but during the summer of 2020, the Turkish state borrowed in USD in one of the most extraordinary tempos in the country’s history.

The final significant moment that you can see in the graph is December 2021 volatility, which produced the lowest levels of reserves attained in the history of the CB and pushed for the foreign-exchange protected lira deposit regulation.

In this vein, a more proper answer to how the CB got creative needs to point out the persistence of attempts to lower the tempo of currency depreciation. Even when the previous Minister of Finance, the mostly ridiculed Albayrak, pointed out that Turkey was moving to a cheap lira plateau in 2020, there were several FX interventions to slow down the loss of value.

This account helps understand the “creativity” of CB until mid-2021. Still, it is not sufficient to clarify the controversy of the late 2021 move to the New Economic Model, which explicitly suggested that Turkey would become a current account surplus country in the medium term, if not in early 2022, with the help of new incentives, cheap labour and depreciated currency (the state managers used more fancy words, such as competitiveness and boosting exports).

Wait for it

Despite this branding (New Economic Model) being used before in 2020, it was made official by the previous aide of Albayrak in late 2021, today’s as-much-ridiculed Minister of Finance Nebati. The only logical explanation is that the power bloc’s developmentalist wing, symbolized by the state parasites and labour-intensive new exporters, consolidated their newly gained upper hand position amid turbulence and perennial crises. The state managers were convinced that it was time to let the Lira lose more value and turn it into the pillar of a new orientation. But to avoid hyperinflation, monetary authorities had to stop the lira’s loss of value at the same time (once again in December 2021).

Today’s CB has no way to overcome the hurdles of the no reserves era but rather wait. Wait for the minimization of the current account deficit, wait for the increase of interest in lira-denominated assets, wait for the end of supply chain shocks… This is hard to swallow and express, so it leads to new absurdities, such as the CB’s monetary policy council referring to forthcoming global peace as possibly helping them control inflation (Council meeting, March 17, 2022).

Hugging like a pro

In the meantime, Erdogan and his entourage are working hard to establish new connections and buy more time until the 2023 plebiscite (it is not fair to call the electoral process in Turkey elections).

But make no mistake, the new foreign policy orientation of the country (which is summed up by photos of Erdogan hugging his archenemies) is more related to the energy agreements and new lines of credit and financial support for some sectors, not the CB. The CB is slightly paralyzed as the money managers try to determine a competitive exchange rate that will make new exporters content but not push for higher inflation, which already skyrocketed to 61 percent in March 2022 (this is the official and not-so-reliable data, the official inflation rate does not sufficiently represent the deteriorating living standards of the population).

The CB is failing, together with the New Economic Model (2022 version) of the Erdogan administration. Amid the war of neighbouring countries, higher energy prices, (premature or not) global financial tightening steps, and a ruling bloc determined to achieve higher than average growth against this background, it does not come as a surprise.